MSMEs, or micro, small, and medium enterprises, are usually regarded as the mainstay of modern economies. They are responsible for a significant part of the global workforce, being at the forefront when it comes to innovation, besides helping to keep the competition alive to benefit the end consumer. Moreover, the distribution of wealth has been made easier as a consequence of all these factors. However, on the other side, these businesses have not been able to get access to traditional loans, which, in turn, has made it hard for them to grow and cope with the adverse conditions. The good news is that the trend is changing gradually, thanks to the digital lending that is providing novel ways of overcoming the financial support challenges that these enterprises have been encountering.

Let’s take a closer look at this paradigm shift in the Indian economy.

Pre-Digital Lending Era

MSMEs form a silent yet impactful sector that remains largely underutilised in the Indian economy and faces credit gaps. The primary reason for the persistent credit gap between MSMEs’ demand and supply is lenders’ scepticism about the borrowers’ creditworthiness, as borrowers often lack reliable data on whom to lend to. This uncertainty causes banks and other lending institutions to remain very cautious in their lending practices, usually favouring existing clients perceived as less risky. Here’s a detailed look at this issue, known as information asymmetry.

Information Asymmetry

The information asymmetry that existed between lenders and MSME borrowers was the biggest challenge. Conventional financial institutions primarily use structured, historical data, such as financial statements, audited balance sheets, and considerable credit histories, to evaluate risk.

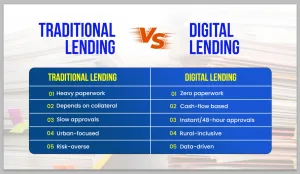

The issue begins with informality. A great majority of MSMEs, particularly micro and small businesses, operate informally or semi-formally, devoid of formal accounting records (like sophisticated ERP systems or certified financial statements) and a considerable formal track record. This lack of ‘paper trail’ made risk assessment by traditional banks impossible through their quantitative models, as banks would have to turn to more subjective, less precise, and consequently, more unreliable approaches.

Digital footprints added to the lack of informality, as in the era before digitalisation, most business transactions were carried out either through cash or manually recorded on paper. Also, even in existing records, they were still not in a large, decentralised financial institution’s easy and trustworthy evaluative structure. The lack of data was a reason for the high-risk perception that lenders assumed as a direct consequence.

Moreover, being new to credit, newly established startups and small entities had to face automatic denial of credit just because they didn’t possess any evaluated formal credit history. The very mechanism intended to measure a company’s creditworthiness was driving away the most dynamic section of the entrepreneurial ecosystem.

Collateral Requirements

Conventional lending has always been about having asset-backed collateral, like real estate or secured assets, to back up loans. However, many modern micro, small, and medium enterprises (MSMEs), especially in the service and digital sectors, operate in an asset-light way. They might possess valuable intellectual property or have intricate business processes, but often lack the significant physical assets that traditional financial institutions look for.

On top of this, lenders tend to be risk-averse, seeing the MSME sector as high-risk due to factors like unpredictable cash flows and high failure rates, combined with the challenge of verifying records. This has led banks to stick to their strict lending policies, favouring large corporations with steady revenue and plenty of collateral instead. As a result, the MSME segment often gets overlooked, partly because processing numerous small loans is just too costly for their existing models.

High Transaction Costs and Geographic Exclusion

For a lot of small business owners, the process of getting a loan from a conventional source has been like ascending a rocky peak. The whole procedure can be very tedious, with an unending amount of paperwork, numerous trips to the bank, and waiting for what feels like an eternity to get the approval. It is a very challenging path to walk on, particularly when you are already busy with the daily operations of your business.

Moreover, it is a much harder way for those who live in rural or semi-urban areas. The limited availability of bank branches in their vicinity makes it almost impossible for them to acquire, thus leaving many diligent entrepreneurs feeling neglected and unsupported. These small ventures are the backbone of local communities and play a crucial role in maintaining the flow of money in the local market; however, crediting institutions often find ways to make them less assisted. It shouldn’t be that hard for the passionate and committed ones.

Entry of Digital Money Lending

With the dramatic rise of FinTech and digital lending platforms, the times when the previously mentioned structural challenges stifled the market are finally over. The current generation of innovators is taking full advantage of data science, non-stop connectivity, and state-of-the-art digital infrastructure to come up with a credit delivery system that is not only agile and scalable but also extremely liberating in terms of access.

One of the revolution’s major components is the absolute risk assessment transformation, an envisioning of letting go of the tedious process of asset-based evaluations and mountains of paperwork. The digital lenders are now presenting their cash-flow-based underwriting models as the new and preferred option, already gaining some ground over the centuries-old artefact of product-based radical margin and exhaustive credit histories. They put their trust, however, in nothing other than the high-tech algorithms and the very essence of alternative data.

The acceptance of the digital traces of small and medium enterprises is one of the most thrilling aspects of the new method. Daily, these businesses, through their operations, produce huge amounts of data, and their existence is quite unaware of the digital lenders who are now ready to access it. The banks on one side of the market will conduct real-time analysis of clients’ daily transactions, which will be communicated through their bank statements, in order to track their sales on the main payment gateways and e-commerce behemoths like Amazon and Shopify. Needless to say, such insights are invaluable. This implies that lenders not only take on risks but also take the steps towards an MSME era where loans are not just awards but also the empowerment of dreams and the driving of growth through previously unimaginable ways.

Moreover, technology has opened access to tax and utility records as well as facilitated the use of digital platforms for GST filings and utility payments to demonstrate the business’ resilience. One can even unravel the complex network of supply chain data in such a way that the connections between buyers and sellers give away the trustworthiness and durability of the financial health. Envision how a strong digital presence through social media and website traffic generates a heartbeat for your business, which is its sign of life and growth.

The dynamic algorithms can help us not only to build a credit scoring system that is quicker but also more precise than ever before. And this is about empowerment, not just numbers! It allows lenders to give their support to businesses that do not have the traditional credit history confidently by analysing their operating rhythms and transactional data footprints. What is more, we can spot warning signs that are early, getting the cash flows monitored in real time to catch the signs of financial distress before they grow into crises. It is a proactive approach that not only lessens the risk of the portfolio but also provides customised repayment plans, enabling businesses to grow even in hard times.

Impact on MSME Growth and Sustainability

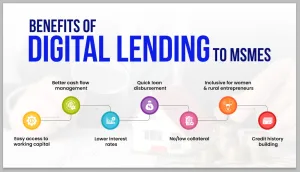

Digital lending has the potential to alter the landscape of micro, small, and medium enterprises (MSMEs) completely by providing them with the necessary support to grow and prosper. When such businesses are given access to timely and affordable capital, they can not only operate to survive but also strive for substantial growth. Loans may be used for the purchase of new machines or the leasing of larger areas, which eventually results in the company being able to produce more. Additionally, they would be financially stable enough to hire an IT company to help them streamline their processes. This financial assistance further enables them to keep track of stock levels, advertise their goods, and even enter new markets without being encumbered by cash flow problems.

What is most promising is that digital lending not only makes credit accessible to the traditional clientele but also to those formerly considered unbankable. It reaches those diligent businesspeople situated far away from the financial centres, especially women and small traders, thus bringing about a much wider range of economic activities. Lenders, by motivating them to register and make use of digital transactions, assist them in establishing a financial profile that may eventually lead to better credit choices.

Enhanced Cash Flow

Digital solutions are a great support for the MSMEs, which are the most affected businesses, helping them to manage the fluctuations of business. Custom-made loans can relieve cash flow problems, thus making it easier to survive the waiting period for payment from buyers. Not only do various platforms give financial backing, but they also provide resources and educational programs to increase the financial literacy of their users. This openness creates trust, which enables the owners of MSMEs to make wise choices and prevent falling into the traps of expensive loans. In the end, not only the digital lending but also the finance issue is about empowering people and building up the future for their businesses and communities.

The Future Path

The future requires collaboration between FinTechs and banks that are also key drivers of India’s future. Also, the investment in both offline and digital literacy for MSMEs is going to be our key. What we can envision is a vigorous, functioning and all-inclusive financial ecosystem where every business that can make it, regardless of its size or location, can access the capital it needs for expansion with ease. The future holds great possibilities, which depend on the hard work done together by both the public and private sectors.